The VA Loan is a powerful mortgage option that has helped more than 22 million veterans, active duty military members and their families, purchase homes and achieve their American dream of homeownership. The program was created in 1944 and is guaranteed by the U.S. Department of Veterans Affairs (VA).

This mortgage program features many amazing benefits, including its no down payment advantage, relaxed eligibility requirements, and competitive interest rates issued by VA-approved lenders. The VA Loan continues to serve as a lifeline for many military home buyers who may find it difficult to be qualified for a regular mortgage because of tough credit standards and down payment requirements.

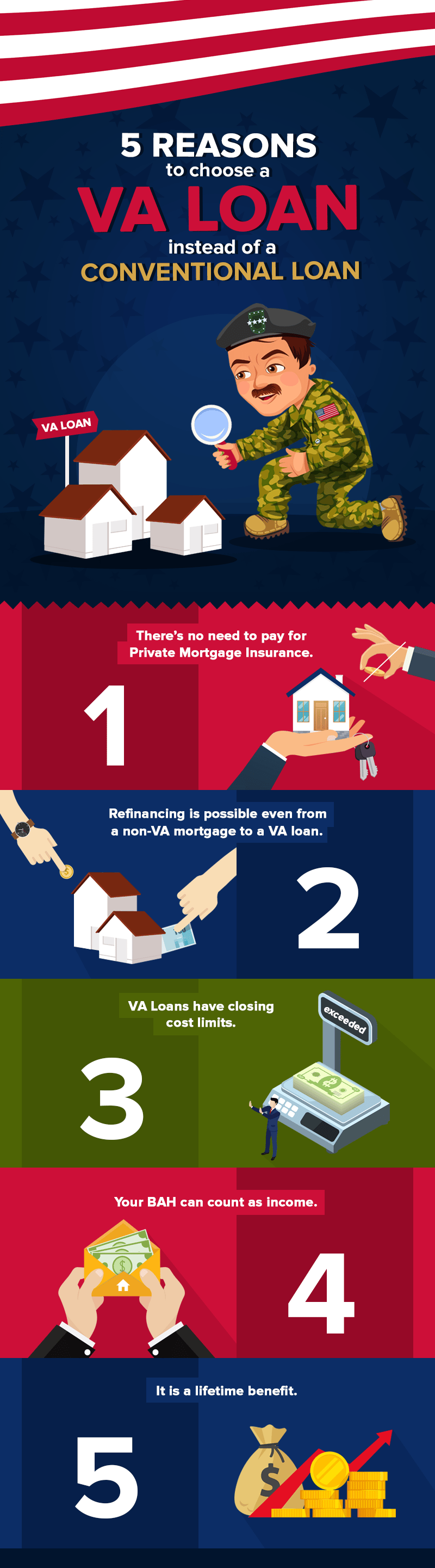

Likewise, here are some of the most attractive perks of VA loans that are simply not available in conventional mortgages and other government-backed loans:

1. There's No Need to Pay for Private Mortgage Insurance

One great thing about VA loans is that borrowers are not required to pay a monthly mortgage insurance unlike in conventional and FHA mortgages. In a conventional loan, borrowers need to pay for Private Mortgage Insurance (PMI) if they pay less than a 20 percent down payment. The PMI protects the lender just in case a borrower defaults on the loan. Meanwhile, FHA loans come with both an upfront mortgage insurance premium and an annual premium which can be paid over the life of the loan and will be added as part of your monthly mortgage insurance.

In a VA home loan, the mortgage is being insured by the federal government so veterans can save thousands of dollars in mortgage insurance costs. With this strong government backing, lenders are even more encouraged to keep closing and origination costs low. The less-risk factor also allows lenders to become more flexible on credit and other lending standards, granting more veterans the opportunity to be eligible for a mortgage.

2. Refinancing is Possible Even From a Non-VA Mortgage to a VA Loan

VA loans do not only prove to be available for new home purchases. In fact, refinancing from a non-VA mortgage to a VA loan is even possible and available for financially qualified borrowers. Those who wish to take advantage of this option will need to find a participating VA lender who is willing to do the transaction.

Likewise, VA loans can be refinanced through the VA Interest Rate Reduction Refinance Loan (also known as the VA IRRRL). The IRRRL can help current military homeowners refinance their existing mortgages to earn a lower interest and have a lower monthly mortgage payment. This VA streamlined program provides exceptional benefits such as the no appraisal requirement, no out-of-pocket costs, no income or credit report verification, and allows refinances of up to 100 percent of the home's value. Don't be afraid to ask a participating VA lender about this VA IRRRL option to find out if you’re eligible.

3. VA Loans Have Closing Cost Limits

While all mortgages automatically come with fees and closing costs, the VA limits the closing costs that lenders can charge veterans. Veterans and military members who will be financing their homes through a VA loan have the flexibility to negotiate expenses with lenders. They are also free to research the closing costs, rates, and mortgage terms provided by lenders.

Some costs and fees associated with a mortgage can also be covered by other parties in the transaction. For an instance, a VA borrower can certainly ask a seller during the negotiation process to pay all of their loan-related closing costs and other expenses, such as prepaid taxes and insurance. These precautions help make homeownership entirely affordable and possible for qualified home buyers.

4. Your BAH Can Count as Income

The Basic Allowance Housing or BAH is one of the several VA benefits available to eligible service members. BAH payments are given monthly to those who are not provided housing by the government or those who are not living in government-issued headquarters. This allowance is intended to fund housing costs so lenders can definitely count BAH as an effective income source. It will help active duty members to qualify for higher loan amounts, and they can also use it to pay for their monthly mortgage costs. The amount a veteran or military member receives for BAH is based on rank, years of service, pay grade, number of dependents, and duty location.

5. It is a Lifetime Benefit

One of the most unbeatable benefits of a VA mortgage program: you can use it over and over again throughout your lifetime. It's contrary to a common misconception that it is only a one-time benefit. It means veterans who have used it decades ago to purchase a property are still eligible if they want to use it today.

It's even possible for borrowers to have more than one VA loan at the same time. You don’t necessarily have to pay back your current VA loan in full in order to be eligible for a new one. It’s especially helpful for military members who have a VA mortgage from their current duty station but need to make a Permanent Change of Station (PCS) move to another part of the country.

Because of these astounding benefits, the VA mortgage program remains as one of the safest loans in the market. Through the VA guarantee, veterans are not only getting their dream homes, but it also helps them keep their homes and avoid foreclosure.